SMM March 27, 2025:

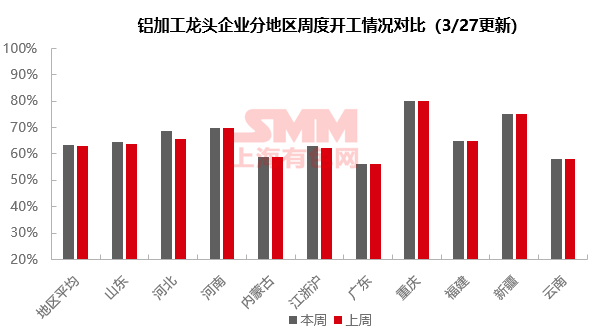

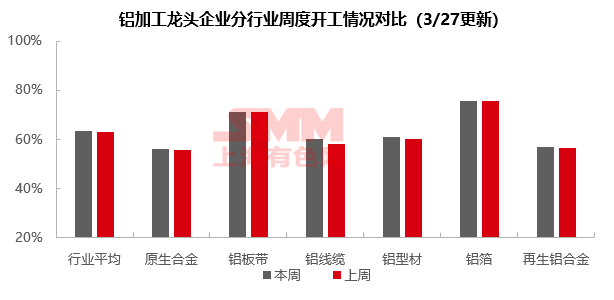

This week, the operating rate of leading domestic aluminum downstream processing enterprises rose 0.6 percentage points WoW to 63.4%. By sector, aluminum wire and cable and PV extrusion performed well, mainly driven by accelerated power grid investment and concentrated PV module deliveries. Aluminum plate/sheet and strip and aluminum foil maintained high levels, with the former benefiting from accelerated destocking by enterprises and the latter relying on policy dividends for NEVs and home appliances. Primary alloy and secondary alloy saw slight increases in operating rates but lacked momentum, constrained by inventory pressure and losses. Overall, accelerated power grid deliveries, concentrated PV module deliveries, and the implementation of special bond projects are expected to support the operating rates of some sectors. However, caution is needed regarding the potential suppression of downstream demand by high aluminum prices, export policy risks, and weaker-than-expected demand in the real estate chain. In the short term, the operating rate of aluminum downstream processing will continue to show a steady and slow upward trend, with SMM predicting a 0.3 percentage point increase to 63.7% next week.

Primary Aluminum Alloy: This week, the operating rate of leading domestic primary aluminum alloy enterprises rose slightly by 0.2 percentage points to 56.0%, with the industry's recovery momentum slowing marginally. On the supply side, although most enterprises maintained stable production, the continued loose supply of circulating goods, coupled with high in-plant and downstream raw material inventories, significantly limited the industry's production increase. On the demand side, weak new order releases and high aluminum price fluctuations suppressed demand, with downstream risk aversion sentiment rising and rigid procurement maintained. Spot market activity remained sluggish. SMM expects the industry's operating rate to continue a mild rebound next week, but caution is needed regarding the negative feedback effect of high aluminum prices on demand.

Aluminum Plate/Sheet and Strip: This week, the operating rate of leading aluminum plate/sheet and strip enterprises remained stable at 71%. Production rhythms of sample enterprises showed no significant changes, continuing steady production. With aluminum prices fluctuating upward, leading enterprises accelerated destocking. However, terminal customers' fear of high prices also increased, with orders and cargo pick-ups mainly for rigid demand. If aluminum prices continue to run high and break the 21,000 mark, it may further suppress downstream order and pick-up enthusiasm, thereby affecting enterprise operating rates. The operating rate of leading aluminum plate/sheet and strip enterprises is expected to remain stable or slightly increase in the short term.

Aluminum Wire and Cable: This week, the operating rate of leading domestic aluminum wire and cable enterprises was 60%, up 2% WoW, maintaining an upward trend. In terms of orders, power grid investment continued to accelerate, with related orders coming in continuously. On March 21, the second batch of material tenders for power transmission and transformation was officially announced, involving 147,000 mt of aluminum conductor and ground wire orders, to be delivered starting June this year. As March ends, the power grid project delivery phase in April is approaching, with enterprise operations remaining prosperous. The industry's operating rate is expected to continue rising in April.

Aluminum Extrusion: This week, the operating rate of the aluminum extrusion industry rose slightly by 1 percentage point WoW to 61%, with sub-sectors continuing to diverge. In industrial extrusion, leading automotive extrusion enterprises maintained an operating rate of over 80% with orders from the NEV industry chain. However, according to SMM surveys, some small and medium-sized building material enterprises that had previously ventured into industrial extrusion reported that automotive extrusion orders were increasingly concentrated in leading enterprises due to complex process certifications and significant equipment investments. Some SMEs faced severe product homogenization, with industrial production lines idling this week. In PV extrusion, despite continued pressure on processing fees, mainstream PV extrusion enterprises maintained full production due to the concentrated delivery period from March to April. In construction extrusion, some enterprises reported a recovery in public construction orders due to the launch of special bond projects (e.g., high-speed rail, industrial parks), with construction extrusion operating rates slightly increasing this week. However, demand for civil building materials remained suppressed by slower real estate completions, with operating rates for window, door, and aluminum formwork extrusion enterprises still low. SMM will continue to track destocking rhythms during the traditional peak season, focusing on the efficiency of demand transmission from NEVs and PV installations and the actual boosting effect of local government special bonds on infrastructure projects.

Aluminum Foil: This week, the operating rate of leading aluminum foil enterprises remained stable at 75.7%. On the macro front, the trade-in policy continued to drive stable output of aluminum foil products related to NEVs and home appliance end-use consumption, such as brazing foil, battery foil, and air-conditioner foil, supporting the overall aluminum foil industry's operating rate. On the other hand, India's imposition of anti-dumping duties on Chinese aluminum foil may lead to a direct decline in exports to India in the short term, further increasing pressure on China's overall aluminum foil exports and adding some instability to the operating rates of leading aluminum foil enterprises.

Secondary Aluminum Alloy: This week, the operating rate of leading secondary aluminum enterprises rose slightly by 0.4 percentage points WoW to 56.9%. Currently, orders for large secondary aluminum enterprises are moderate, with operating rates slightly increasing, but overall market demand has not shown significant recovery, and enterprise finished product inventories have increased. Additionally, the price drop of finished alloy ingots exceeded the adjustment in raw material prices, leading to expanded theoretical losses in the industry. Faced with production losses and inventory pressure, some enterprises began considering production cut plans. In the short term, the industry's operating rate is expected to remain stable or slightly decline.

》Click to view SMM Aluminum Industry Chain Database

(SMM Aluminum Team)